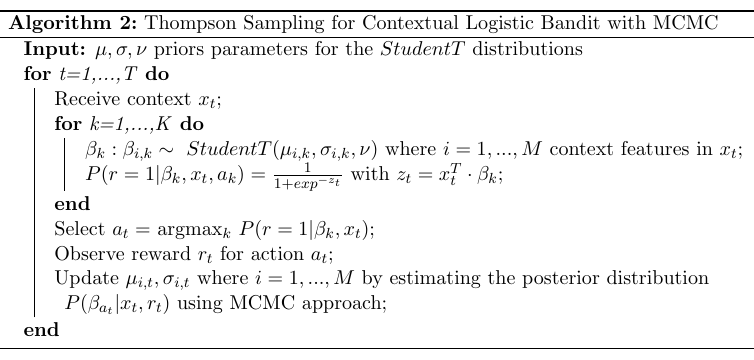

Contextual Multi-Armed Bandit

For the contextual multi-armed bandit (cMAB) when user information is available (context), we implemented a generalisation of Thompson sampling algorithm (Agrawal and Goyal, 2014) based on NumPyro.

The following notebook contains an example of usage of the class Cmab, which implements the algorithm above.

[1]:

import numpy as np

from pybandits.cmab import CmabBernoulli

from pybandits.model import BayesianNeuralNetwork, BnnLayerParams, BnnParams, FeaturesConfig, StudentTArray

/home/runner/.cache/pypoetry/virtualenvs/pybandits-vYJB-miV-py3.10/lib/python3.10/site-packages/tqdm/auto.py:21: TqdmWarning: IProgress not found. Please update jupyter and ipywidgets. See https://ipywidgets.readthedocs.io/en/stable/user_install.html

from .autonotebook import tqdm as notebook_tqdm

[2]:

n_samples = 1000

n_features = 5

First, we need to define the input context matrix \(X\) of size (\(n\_samples, n\_features\)) and the mapping of possible actions \(a_i \in A\) to their associated model.

[3]:

# context

X = 2 * np.random.random_sample((n_samples, n_features)) - 1 # random float in the interval (-1, 1)

print("X: context matrix of shape (n_samples, n_features)")

print(X[:10])

X: context matrix of shape (n_samples, n_features)

[[-0.29510423 0.1068003 -0.43523171 -0.69415258 0.02661787]

[ 0.55093182 0.43291438 -0.66035325 -0.06429803 0.11879739]

[-0.76834155 0.63006007 -0.3286156 0.81764852 -0.96857704]

[-0.06774331 0.8558794 -0.30714485 -0.980672 -0.62003066]

[-0.433614 -0.99960589 -0.14863463 -0.84700138 0.3058156 ]

[-0.68251017 -0.40540145 -0.24761987 -0.51004182 0.748183 ]

[-0.77390573 -0.67027872 0.52795189 0.24742719 -0.0752349 ]

[-0.39993445 0.27510234 0.86712322 0.45277544 -0.00977359]

[-0.92392614 -0.72671577 -0.51134801 -0.99505028 0.9767449 ]

[-0.6603465 -0.6826477 -0.94683999 -0.06060249 -0.8213706 ]]

[4]:

# define action model

bias = StudentTArray.cold_start(mu=1, sigma=2, shape=1)

weight = StudentTArray.cold_start(shape=(n_features, 1))

layer_params = BnnLayerParams(weight=weight, bias=bias)

model_params = BnnParams(bnn_layer_params=[layer_params])

feature_config = FeaturesConfig(n_features=n_features)

update_kwargs = {"num_steps": 100, "batch_size": 128, "optimizer_type": "adam"}

actions = {

"a1": BayesianNeuralNetwork(

model_params=model_params,

feature_config=feature_config,

update_kwargs=update_kwargs,

),

"a2": BayesianNeuralNetwork(

model_params=model_params,

feature_config=feature_config,

update_kwargs=update_kwargs,

),

}

We can now init the bandit given the mapping of actions \(a_i\) to their model.

[5]:

# init contextual Multi-Armed Bandit model

cmab = CmabBernoulli(actions=actions)

The predict function below returns the action selected by the bandit at time \(t\): \(a_t = argmax_k P(r=1|\beta_k, x_t)\). The bandit selects one action per each sample of the contect matrix \(X\).

[6]:

# predict action

pred_actions, _, _ = cmab.predict(X)

print("Recommended action: {}".format(pred_actions[:10]))

Recommended action: ['a1', 'a1', 'a2', 'a2', 'a1', 'a1', 'a2', 'a2', 'a2', 'a2']

Now, we observe the rewards and the context from the environment. In this example rewards and the context are randomly simulated.

[7]:

# simulate reward from environment

simulated_rewards = np.random.randint(2, size=n_samples).tolist()

print("Simulated rewards: {}".format(simulated_rewards[:10]))

Simulated rewards: [0, 0, 0, 1, 0, 1, 1, 0, 0, 1]

Finally, we update the model providing per each action sample: (i) its context \(x_t\) (ii) the action \(a_t\) selected by the bandit, (iii) the corresponding reward \(r_t\).

[8]:

# update model

cmab.update(context=X, actions=pred_actions, rewards=simulated_rewards)